On November 12, 2024, Vietnam’s Ministry of Finance initiated a public consultation on the Draft Decree that provides guidance on implementing the Resolution No. 107/2023/QH15 (“Resolution 107”). This resolution introduces additional Corporate Income Tax (“CIT”) measures, in line with the Global Anti-Base Erosion (“GloBE”) Rules.

The Draft Decree outlines the application of the Qualified Domestic Minimum Top-up Tax (“QDMTT”) and the Income Inclusion Rule (“IIR”), marking a significant step in Vietnam’s alignment with global minimum tax (“GMT”) standards.

This article provides an overview of the GMT and Draft Decree’s key provisions and implications for businesses, along with the challenges we expect when collecting top-up tax under the QDMTT and IIR regimes.

1. Overview of the GMT

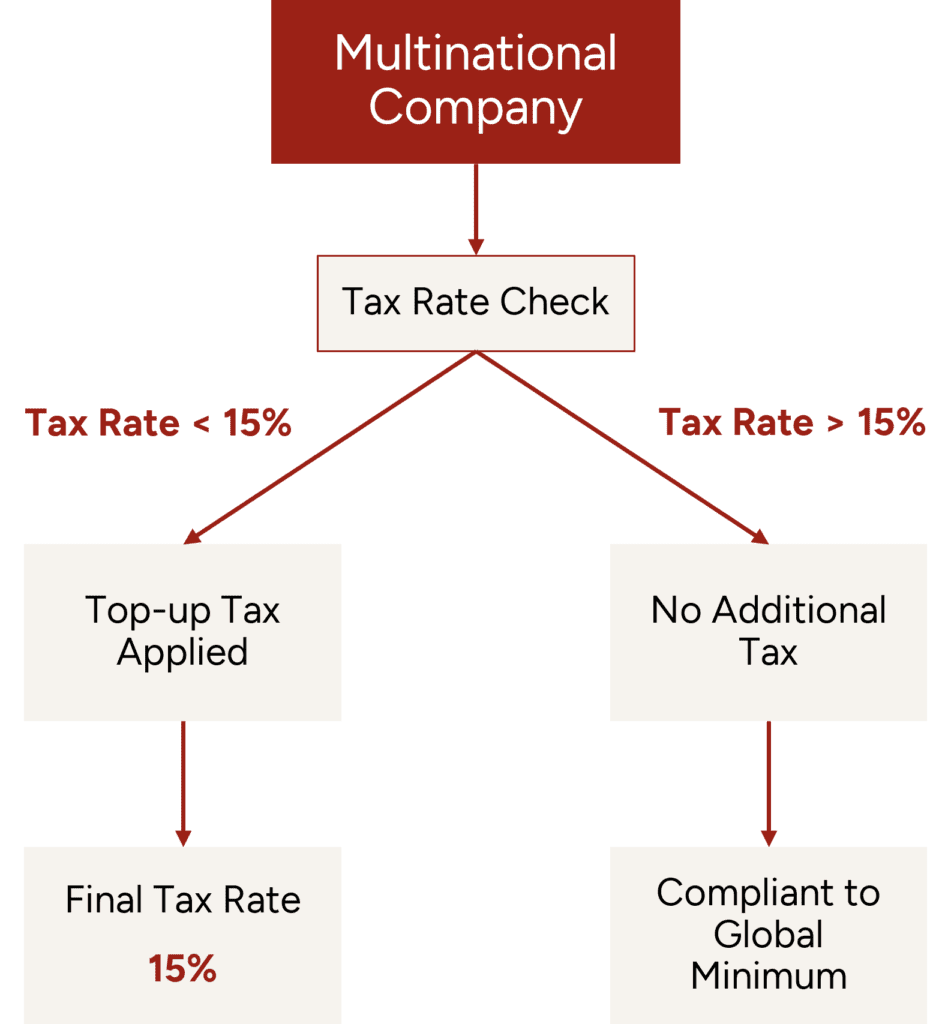

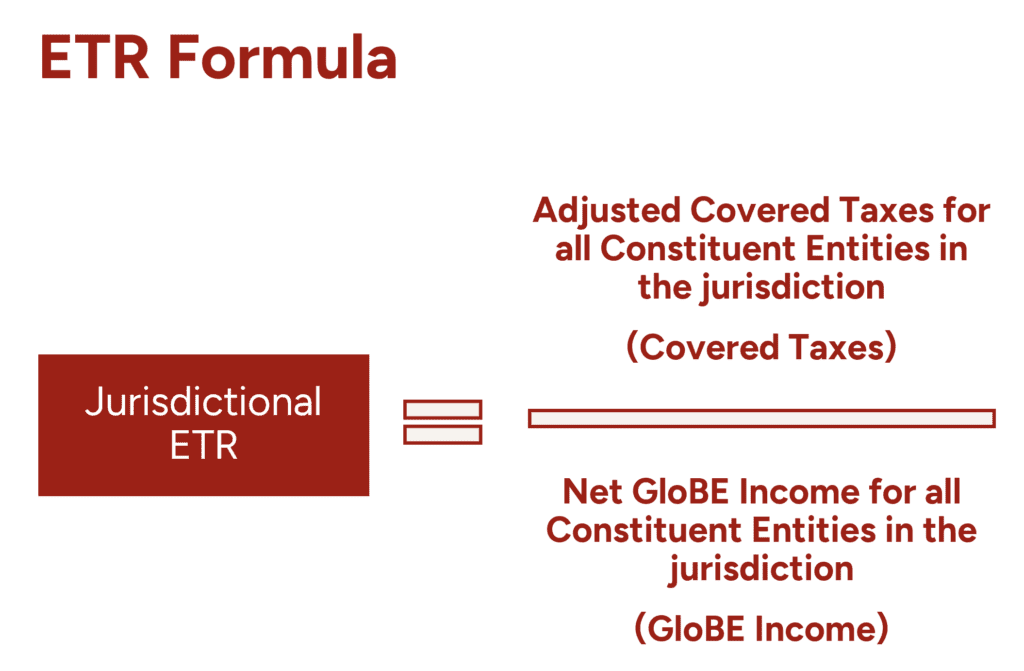

The OECD’s global minimum tax (also known as Pillar Two) establishes a 15% minimum effective tax rate (“ETR”) for large multinational companies (“MNCs”) with annual revenue exceeding €750 million. If a MNC pays less than 15% in any jurisdiction, its home country can levy additional tax to ensure the 15% minimum rate is met, preventing tax shifting through low-tax jurisdictions.

From the Draft Decree, we note that Vietnam emphasizes the importance of the QDMTT provisions compared to the IIR regulations. This approach contrasts with other countries’ implementation of the GMT frameworks, perhaps because Vietnam wishes to preserve its primary right to tax low-taxed income generated domestically, ensuring that revenue is not shifted to foreign jurisdictions under the IIR. This safeguards Vietnam’s domestic tax base and reduces the risk of tax revenue loss.

2. Key Features of the Draft Decree

Qualified Domestic Minimum Top-up Tax (QDMTT):

The QDMTT is a tax mechanism introduced by the Global Minimum Tax (GMT) framework, under the OECD’s Pillar Two rules, to ensure that multinational companies (MNCs) pay a 15% minimum effective tax rate (“ETR”) on their profits in each jurisdiction where they operate.

If the ETR in a country falls below 15%, a “top-up tax” must be applied to bring the total tax paid up to the minimum 15% threshold. The QDMTT allows countries to collect this top-up tax locally, rather than allowing other jurisdictions to claim it.

Key Details about QDMTT in the Draft Decree:

- Scope of Application:

– Constituent Entities (CEs) of MNC with annual consolidated revenue of EUR 750 million or more in at least two of the four preceding fiscal years.

– Both inbound MNCs (foreign parent entities with operations in Vietnam) and Vietnamese headquartered MNCs are subject to the draft decree application.

- Rules of Application:

- Filing Obligations: Taxpayers must prepare and submit:

– GloBE Information Return.

– Supplementary CIT return with explanations for variances due to different accounting standards (if any).

- Filing deadlines:

– 12 months after the fiscal year-end for the QDMTT filing package.

– The Ultimate Parent Entity (“UPE”) must designate a Filing CE within 30 days of the fiscal year-end. If not, the tax authority will appoint the CE having the largest total asset value.

- The Safe Harbour provisions under the GMT framework aim to give time to MNCs to adapt with the new regulations and shall be effective from the financial year ending in 2024. During the Safe Harbour period, there shall be no additional top up tax if:

– The MNC group reports total revenues below EUR 10 million and a profit before tax of less than EUR 1 million; or if the group incurs a loss, in the relevant jurisdiction, according to its qualified CbCR for the fiscal year.

– The MNC group applies a simplified effective tax rate that meets or exceeds the transition rate for the fiscal year. The transition rates are set as follows: 15% for fiscal years starting in 2023 and 2024; 16% for fiscal years beginning in 2025; and 17% for fiscal years starting in 2026.

– The profit before tax of the MNC group in the jurisdiction is either equal to or lower than the amount for substance-based income exclusion, as determined under the GloBE rules, for constituent entities based in that jurisdiction, as reported in the CbCR.

3. Implementation Challenges

Vietnam has been relying on tax incentives, such as corporate income tax (“CIT”) holidays, preferential tax rates, and exemptions, to attract foreign investors, particularly in the manufacturing sector and special economic zones (“SEZs”). The introduction of the GMT (with a minimum effective tax rate of 15%) could undermine the effectiveness of these incentives.

However, Vietnam must compete with other developing countries in Southeast Asia to attract foreign-direct investment (“FDI”) and needs to think of other incentives to remain an attractive destination for FDI in the region.

Besides, we anticipate challenges with regard to the GMT’s coordination with other international instruments:

- Harmonization with Domestic Tax and Accounting Laws: While Vietnam has officially adopted IFRS, the tax regulations have not yet been updated to reflect this change and we must continue to rely on the Vietnam Accounting Standards (“VAS”). This may lead to inconsistencies and challenges in adhering to the GMT framework.

- Interaction with Existing Tax Treaties: Vietnam has signed numerous bilateral tax treaties. These treaties may need to be renegotiated or amended to comply with the GMT, which could create legal and administrative hurdles.

- Human Resources: Vietnam will need highly trained tax professionals with expertise in international tax law, transfer pricing, and the GMT framework. These professionals must understand the complex rules for calculating ETRs, including adjustments for deferred taxes, exclusions, and thresholds.

- Technology and IT Systems

- Data Collection and Management: Vietnam will need robust IT systems to collect, store, and analyze financial data from MNCs operating in the country. These systems must be capable of handling large volumes of data and ensuring data accuracy and security.

- Automation Tools: Advanced software tools will be required to automate the calculation of ETRs and ensure compliance with GMT rules. These tools should integrate with existing tax administration systems to streamline processes and reduce manual errors.

- Digital Infrastructure: Vietnam must continue investing in digital infrastructure to facilitate information sharing between tax authorities, MNCs, and international bodies.

4. ASEAN’s adoption of GMT

As of early 2025, Singapore is leading the regional implementation of the global minimum tax, having passed its legislation at the end of 2024 to implement the Minimum Effective Tax Rate (METR) rules from January 1, 2025.

Malaysia has also confirmed its commitment and passed the necessary legislation to implement Pillar Two from 2025.

However, Thailand and Indonesia have taken a more cautious approach – Thailand has announced plans to implement but is still finalizing its legislative framework, while Indonesia has expressed support for the global minimum tax but has not yet set a definitive implementation timeline as they are still conducting impact assessments and stakeholder consultations. These different implementation stages reflect the different economic priorities and tax policy considerations of Southeast Asian countries and economies.

If you require further guidance or support with regard to this matter, please contact the author or our team.

Our team is here to provide expert advice and assistance, ensuring that your organization remains compliant with the latest regulatory requirements and best practices.